What Does This Mean?

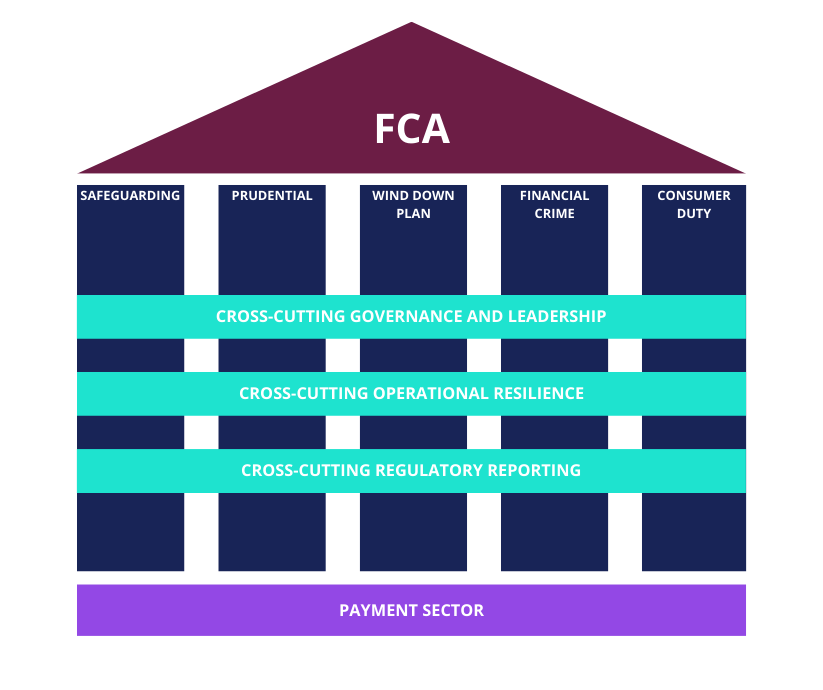

Safeguarding

The FCA is laser-focused on reducing the harm that arises from firm failure. They want to see robust safeguarding arrangements, including documented processes for identifying “relevant funds” for safeguarding, daily reconciliations to ensure correct sums are protected, and bank safeguarding acknowledgement letters on file.

The FCA also reminds firms that are required to have a statutory audit to appoint an auditor for safeguarding and to ensure that the FCA is made aware of any adverse findings or non-compliance.

Prudential

The FCA stresses the need for firms to improve prudential risk management. They remind firms that they need to meet regulatory capital requirements at all times and to plan well ahead to ensure that they have adequate financial resources on an ongoing basis.

Wind-Down Planning

The FCA has found that many companies have not created wind-down plans or have created poorly drafted plans that don’t provide sufficient detail on triggers, practical steps, and the costs of winding down. Firms need to get grips with wind-down planning asap.

Financial Crime

The FCA noted increased evidence of financial crime in the sector and reminds firms of their obligations in relation to AML, fraud, and sanctions.

The FCA also suggest that fraud could increase due to the cost-of-living crisis and they emphasise the need for firms to review and address weaknesses in their fraud systems and to maintain strong due diligence controls.

Consumer Duty

In preparation for the incoming Consumer Duty, the FCA remarks that they continue to see examples of firms not acting in the customer’s best interest. The FCA reminds firms of their need to comply with the Duty and ensure good outcomes for customers.

Cross-Cutting Priorities

The FCA notes that issues such as governance and leadership, including lack of experienced personnel and meaningful due diligence could be contributing to a lot of the regulatory issues in the sector.

They remind firms of the importance of undertaking due diligence on their directors and agents/distributors, building out their Operational Resilience and ensuring that they submit accurate and timely Regulatory Reports or face fines or enforcement action.