Blog

APRIL 2, 2026 • 5 MIN READ

Instant Payments Regulation (IPR) Reporting: What EU PSPs Must Submit by 9 April 2026

Fiona Jelly,

Founder & CEO of Complyfirst

This applies to PIs/EMIs and Banks in the EU

What is the Instant Payments Report (IPR)?

The Instant Payments Report (IPR) is a supervisory statistical return requiring aggregated data on SEPA Instant usage (i.e. volumes, values and operational metrics relating to instant transfers) that must then be submitted to a firm’s national competent authority.

The key point of the IPR is that regulators want transparency on how instant payments are priced and how often they are rejected, especially due to sanctions screening.

And the first submission, due 9 April 2026, requires four historical reports in one go (2022–2025), which is where the reporting workload really racks up.

Submission is:

- Via your relevant NCA reporting portal (e.g., Central Bank of Ireland Portal)

- In XBRL format

- Due annually by 9 April

It’s also important to note that this is entity-level reporting under Article 15(3) of Regulation (EU) No 260/2012. We’ll come back to this further down the blog on why this is an important consideration.

TL;DR

- What changed: PSPs offering SEPA Instant Credit Transfers must submit a new Instant Payments Report (IPR) under the EBA’s draft ITS on uniform reporting.

- Who is affected: Banks, Payment Institutions (PIs) and E-Money Institutions (EMIs) providing SEPA Instant services across the EU.

- When: First submission due 9 April 2026, including multi-year backfill data (26 October 2022 – 31 December 2025).

- Why it matters: For the first time, regulators get a consistent, EU-wide view of how instant payments are being used, priced, and controlled. In practice, that means they can benchmark you against peers on things like instant payment fees and sanctions-related rejection rates.

Scope: Who Must Report?

Let’s first clarify applicability.

You are in scope if:

- You are a PSP in a euro Member State, or

- You are a PSP in a non-euro Member State offering euro credit transfers,

- And you provide SEPA Credit Transfers (SCT) and/or SEPA Instant Credit Transfers (SCT Inst).

This includes:

- Credit institutions

- Payment Institutions

- E-Money Institutions

The trigger is activity-based.

If you provide SCT Inst, you are in scope.

What are the Backfill Requirements?

This is where the bulk of effort sits for your first IPR submission.

Your first submission requires you to reconstruct and report historical SEPA Instant data back to October 2022 in a structured, regulator-ready format.

It must include aggregated data for:

| Period Covered | Reporting Requirement |

|---|---|

| 26 October 2022 – 31 December 2022 | Aggregated data |

| 1 January 2023 – 31 December 2023 | Annual aggregates |

| 1 January 2024 – 31 December 2024 | Annual aggregates |

| 1 January 2025 – 31 December 2025 | Annual aggregates |

In other words:

Year one = four reporting periods.

From 2027 onward, submissions will cover the preceding calendar year only.

So what does that mean in practice?

If you offer SEPA Instant today, you need to extract and structure historical data going back to October 2022. After this initial backfill cycle, reporting becomes annual.

Home vs Host Reporting (Where Reporting Load Can Quickly Add Up)

Article 15(3) reporting is aligned with ECB statistical approaches, and the rule is clear:

- Parent entities report to their home Member State authority.

- Branches report to the competent authority in their host Member State.

In plain English, this means that if you operate cross-border, you may file multiple reports.

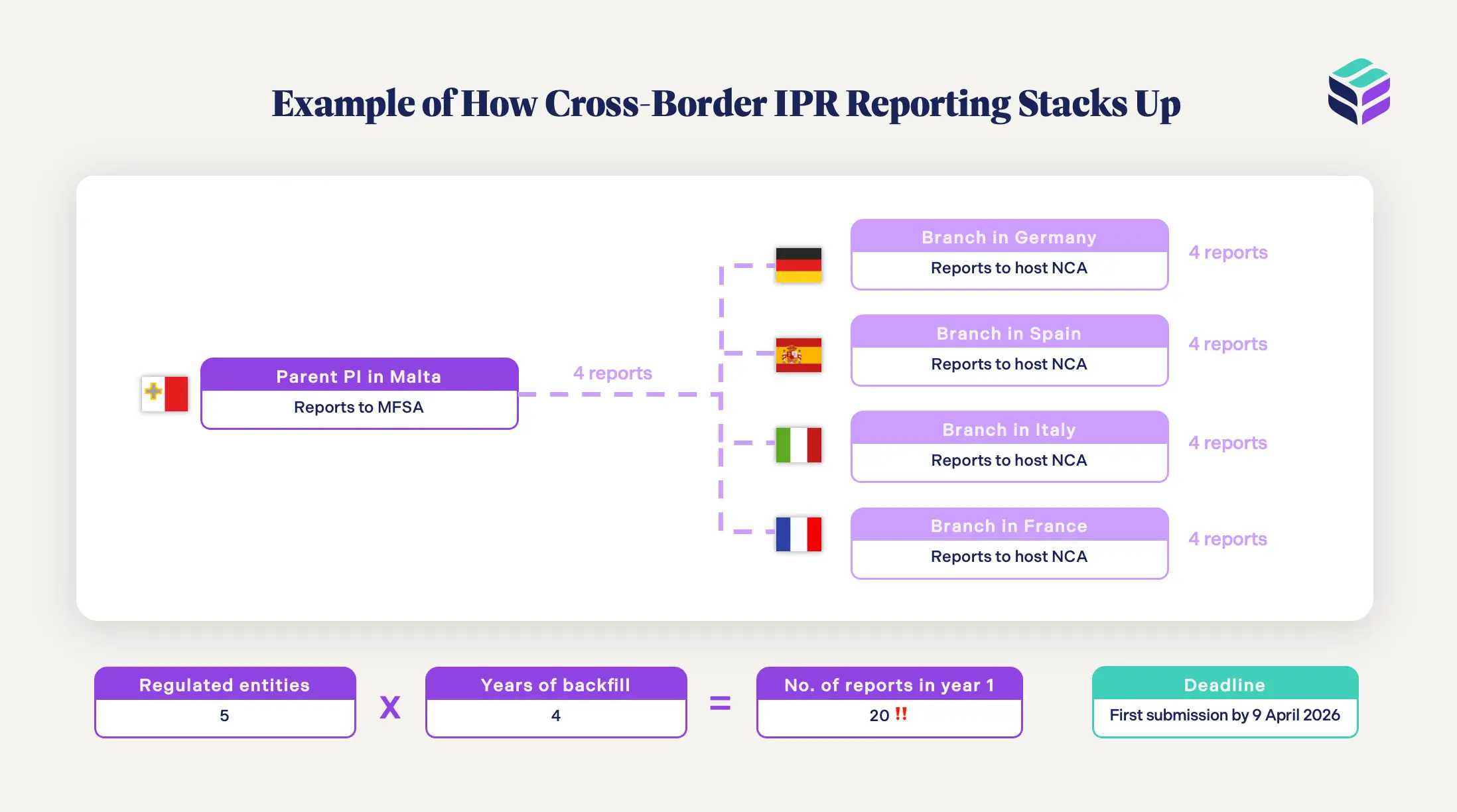

Example of how the impact of the IPR report stacks up quickly:

- Parent PI authorised in Malta → reports to the MFSA (home).

- Branches in Germany, Spain, Italy, France → each branch reports to its host NCA.

Translation: potentially multiple submissions for the same group.

If you have:

- 5 regulated entities

- 4 years of backfill

You are not filing one report.

You may be filing 20 reports in year one.

That is where the operational load sits and what firms need to be aware of.

What Exactly Needs to be Reported? (Filling out the Core Templates)

There are four core templates (six if including non-euro member state firms): volumes, charges, accounts, and sanctions.

| Template | Description |

|---|---|

| Template 1.1 – Volumes | SCT + SCT Inst transfers sent/received, transaction counts and total values, split by national vs cross-border. |

| Template 2.1 – Charges | Fees charged for SCT + SCT Inst sent/received, split by national vs cross-border |

| Template 3 – Accounts | Total number of payment accounts and total account charges (incl. maintenance fees) |

| Template 4 – Sanctions | Number and % of SCT Inst rejected/frozen due to sanctions screening, split national vs cross-border |

Importantly, the templates are linked, so totals and splits must reconcile across them. Supervisors will cross-check.

Steps to Submitting Your IPR

1. Assign Ownership (Entity vs Branch Reporting)

Start with reporting accountability, as in who submits to which authority, i.e. licensed entities report to their home regulator, branches report to their host regulator.

In practice:

- Legal entities report to their home state regulator (e.g. CBI, FCA)

- Branches report to the local host regulator where they operate

What you need to do:

- Map each reporting entity and branch

- Confirm regulator ownership per entity

- Align data flows to reporting responsibility

2. Separate Sanctions-Related Failures from Other Rejections

Next, focus on data classification. Firms must distinguish transaction outcomes, i.e. sanctions-related rejections vs operational or technical failures.

You need to clearly separate:

- Payments rejected or frozen due to sanctions screening

- Payments failed for other reasons (e.g. technical errors, insufficient funds)

What you need to do:

- Review how rejection reasons are captured today

- Standardise classification logic across systems

- Ensure sanctions-related outcomes are clearly identifiable

- Validate historical consistency (back to 2022)

The regulator will expect clean separation and clear logic.

3. Run the Backfill

This is the step most firms underestimate.

You are not submitting one year of data. You are submitting multiple years for your first submission.

So you need to:

- Run full historical extraction

- Test aggregation logic across all periods

- Identify gaps or inconsistencies

- Reconcile outputs against known volumes

Make IPR Submissions Easy with Complyfirst

Complyfirst supports IPR submissions from entity-level reporting and data mapping to continuous validation, XBRL generation, and 1:1 support when you need us.

Here’s how we can help:

- Map entity vs branch reporting correctly, aligned to NCA guidance for backfill submissions

- Support multi-source data ingestion (payments, sanctions, core systems)

- Real-time data validation with clear “how-to-fix-it” steps

- Generate submission-ready XBRL files aligned to NCA taxonomies

- DM us for 1:1 support and get a response in <1hour (yes, even on deadline day).

For a full snapshot of the IPR, you can also watch a video snippet below from Fiona’s EU webinar session, or download a full PDF snapshot right here.

FAQs

The Instant Payments Regulation (EU) is an EU law that amends the SEPA Regulation to standardise and expand the use of instant euro payments across the EU. As part of this, it introduces new obligations for PSPs, including requirements on pricing parity, payment processing timelines, and annual reporting under Article 15(3) to give regulators visibility into instant payment usage, charges, and sanctions-related rejections.

Yes. If you offer SCT/SCT Inst to customers, you’re in scope and must report even if settlement is done via a partner bank.

Yes, the four templates are interlinked, but a bit lighter than DORA. Templates reconcile on totals (SCT vs SCT Inst) and splits (national vs cross-border), but it’s not a beast like DORA (15 interlinking tables!).

Regulators will use it to spot hidden instant-payment charges and/or abnormally high sanctions rejects/freezes, then benchmark you against peers and challenge outliers.

Conclusion

The instant Payment Report is a multi-year data reconstruction exercise combined with ongoing supervisory reporting. With four years of backfill, entity-level obligations, and potential duplication across home and host authorities, the reporting workload stacks up quickly. The real work lies in getting this data aligned. The key is getting your data structured correctly for the first submission so you’re not reinventing the process each year.